Updated June 2026

What Is Collision Coverage Insurance?

Collision coverage repairs or replaces your car after you hit another vehicle, a stationary object like a guardrail or pole, or roll your car over. It applies whether you caused the accident or not, and whether the other driver has insurance or not. You pay your chosen deductible first, then the insurer covers the rest up to your car's actual cash value at the time of the loss. If the repair cost exceeds that value, the insurer declares the car a total loss and pays you the depreciated value minus your deductible.

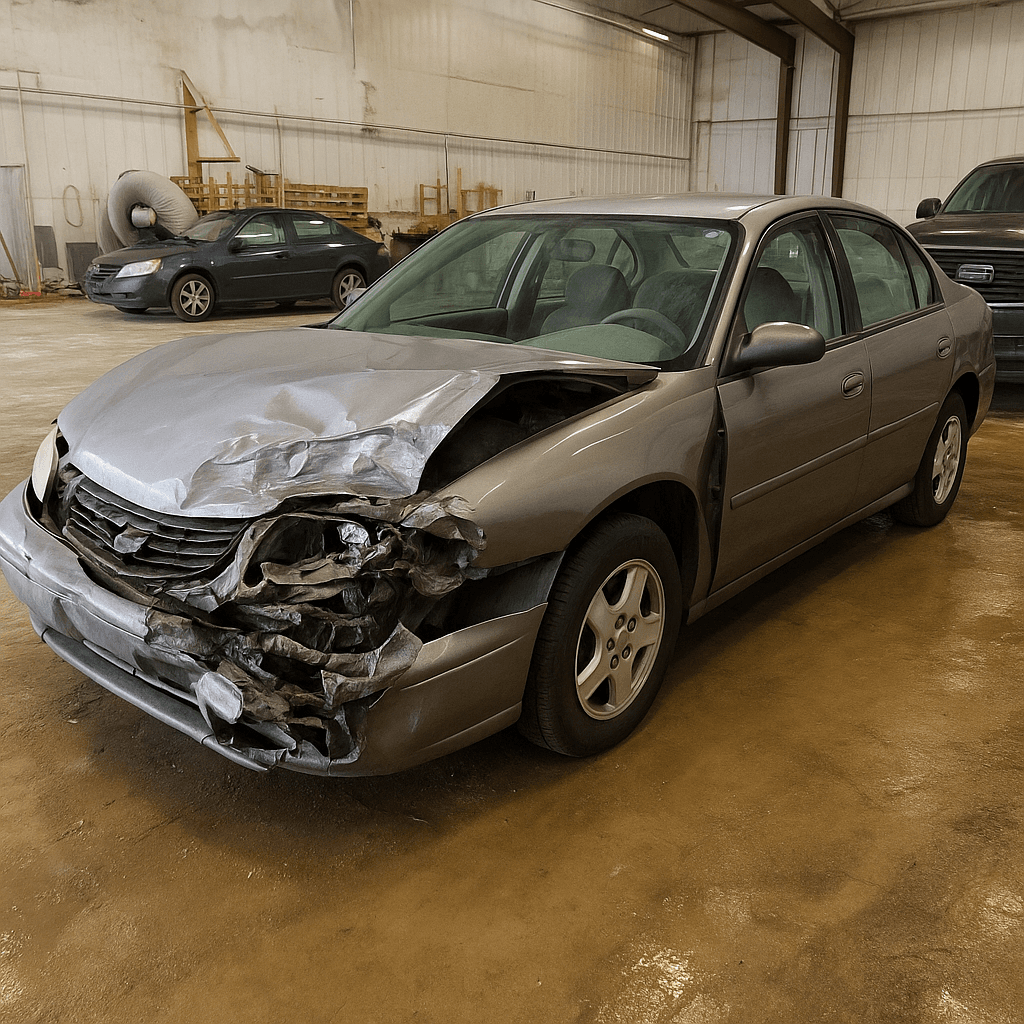

- You tap the brakes too late and hit the car ahead, causing $4,200 in damage to your front bumper, hood, and radiator. With a $500 deductible, collision pays $3,700. The other driver's damage and injuries are covered by your liability policy, not collision. Without collision coverage, you pay the full $4,200 out of pocket.

- A ladder falls off a truck ahead and you veer right into a highway barrier, causing $6,800 in damage to your passenger side. Collision covers this single-vehicle accident. You pay your $1,000 deductible, the insurer pays the remaining $5,800. If you carried only liability, you receive nothing and cover the repair yourself.

- Another driver runs a stop sign, t-bones your car causing $9,500 in damage, and drives off. Uninsured motorist property damage covers this in California if you carry it, but collision also applies regardless of whether you identify the other driver. You pay your deductible, collision pays the rest. If your car is totaled and worth $8,000, collision pays $7,000 after your $1,000 deductible, not the $9,500 repair estimate.

Who Needs Collision Coverage Insurance?

Carry collision if your car is worth more than $5,000 and you couldn't afford to replace it from savings after an at-fault accident. If you're still making loan or lease payments, your lender requires it. Retirees who drive a late-model car in congested areas or on highways daily benefit from collision even if the car is paid off, because repair costs after a moderate accident often exceed $8,000.

Calculate your car's actual cash value using Kelley Blue Book or NADA, subtract your deductible, then divide your annual collision premium by that net payout. If the result is greater than 0.15, you're paying more than 15 cents per dollar of coverage and should consider dropping it. A $2,500 car with a $500 deductible and $480 annual premium yields 0.24 — you'd recover your cost in just over four years only if you total the car, and its value drops every year.

How Much Does Collision Coverage Insurance Cost?

Collision adds approximately $40–$90 per month to your California premium, or $480–$1,080 annually, depending on your car's value, your deductible choice, and your driving record.

- Your car's actual cash value — higher value means higher premiums because the insurer's maximum payout increases.

- Your chosen deductible — selecting $1,000 instead of $250 can cut collision premiums by 30–40 percent.

- Your zip code's collision claim frequency — areas with congested traffic or higher accident rates cost more.

- Your age and driving record — a retiree with 40 years and no at-fault accidents qualifies for lower collision rates than a driver with recent claims.

- Whether you bundle collision with comprehensive — most carriers discount when you carry both on the same policy.